Which of the following Cognitive Biases do you plan on conquering in your 2025 Resolutions to improve your Investment Decisions?

Below is a list of some of the most commonly cited cognitive biases that significantly affect how individuals, investors, and financial professionals make decisions.

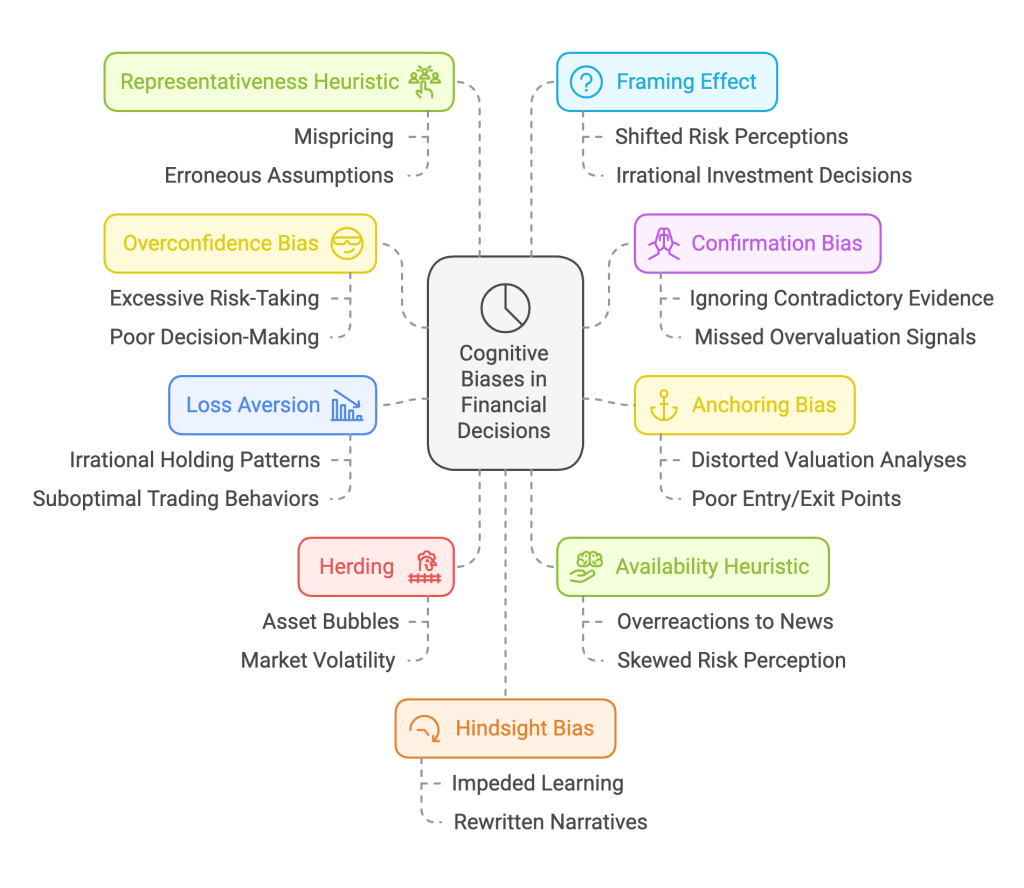

1. Overconfidence Bias

Overconfidence bias refers to the tendency for people to overestimate their abilities, the accuracy of their forecasts, or the precision of their knowledge. In finance, it manifests when traders or investors believe they have superior information or skill relative to others.

Overconfidence can lead to excessive risk-taking, insufficient diversification, and poor decision-making when individuals ignore cautionary signals or fail to consider alternative outcomes.

2. Confirmation Bias

Confirmation bias is the tendency to search for, interpret, and remember information in a way that confirms one’s preconceptions, while giving disproportionately less consideration to contradictory evidence.

Confirmation bias can cause investors to fail to properly reassess their positions and miss clear signals of overvaluation or deteriorating fundamentals.

3. Anchoring Bias

Anchoring bias is the tendency to rely too heavily on the first piece of information (“the anchor”) when making decisions. Subsequent judgments often remain close to this anchor, even if it is arbitrary or irrelevant.

Anchors can distort valuation analyses and cause investors to miss changes in a company’s fundamentals or market conditions, leading to poor entry or exit points.

4. Loss Aversion

Loss aversion, closely related to Prospect Theory, is the tendency for people to prefer avoiding losses over acquiring equivalent gains. Losses are felt more intensely than gains of the same magnitude.

Loss aversion can cause irrational holding patterns and suboptimal trading behaviors, leading to what is sometimes referred to as the “disposition effect” (the tendency to sell winners too soon and hold losers too long).

5. Herding (or Herd Mentality)

Herding is the tendency to follow and mimic the actions of a larger group, regardless of one’s own analysis. Groupthink can lead market participants to make similar decisions and create asset bubbles or crashes.

Herding can inflate valuations beyond reasonable levels or lead to sharp corrections when sentiment shifts, increasing market volatility and systemic risk.

6. Availability Heuristic

This bias occurs when individuals estimate the likelihood of events based on how easily examples come to mind. Recent or dramatic events are overemphasized, while less memorable occurrences are underweighted.

Availability bias can cause overreactions to recent news and skew perceptions of risk and return, sometimes leading to panic selling or euphoric buying.

7. Representativeness Heuristic

The representativeness heuristic is the tendency to judge the probability or frequency of a hypothesis by considering how much it resembles available data or stereotypes, rather than using more rigorous statistical or fundamental analysis.

Relying on superficial similarities can lead to mispricing and erroneous assumptions about future performance, sometimes fueling bubbles and speculative mania.

8. Framing Effect

The framing effect occurs when people respond differently to the same information depending on how it is presented (e.g., as a gain vs. a loss).

How information is presented can shift risk perceptions and lead to irrational investment or divestment decisions.

9. Hindsight Bias

Hindsight bias is the tendency to believe, after an event has occurred, that we would have predicted or expected the outcome. It can lead people to view past events as having been more predictable than they actually were.

Hindsight bias hampers learning from mistakes because investors rewrite the narrative of what they “should” have done without properly examining their flawed assumptions or analyses.

10. Regret Aversion

Regret aversion bias drives individuals to avoid making decisions that could lead to feelings of regret or responsibility for a negative outcome.

Regret aversion can lead to inaction at critical moments (not cutting losses or rebalancing) or chasing performance based on fear of missing out, both of which harm long-term returns.

11. Self-Attribution Bias

Self-attribution bias is the tendency to attribute successful outcomes to personal skill while blaming external factors or luck for failures.

Failing to recognize when luck is involved can hinder objective self-assessment and improvement. It exacerbates overconfidence, reinforcing behaviors that may not be sustainable.

12. Endowment Effect

The endowment effect is the tendency for individuals to value an asset more highly simply because they own it, even if there is no fundamental change in its objective value.

Overvaluation of owned assets can result in holding onto investments that should be sold or missing better investment opportunities.

These cognitive biases demonstrate that financial decision-making is seldom purely rational. Recognizing and understanding them is critical to mitigating their negative effects. Techniques such as checklists, devil’s advocacy, pre-mortems, and other decision frameworks can help finance professionals and individual investors reduce bias and improve long-term outcomes.

By actively striving to identify these biases in our own (and our organizations’) decision-making processes, we can enhance the quality of our financial analysis and investment strategies.

Key References

- Kahneman, D. (2011). Thinking, Fast and Slow.

- Odean, T. (1999). Do Investors Trade Too Much? American Economic Review, 89(5), 1279–1298.

- Tversky, A., & Kahneman, D. (1974). Judgment under Uncertainty: Heuristics and Biases. Science, 185(4157), 1124–1131.

- Nickerson, R. S. (1998). Confirmation Bias: A Ubiquitous Phenomenon in Many Guises. Review of General Psychology, 2(2), 175–220.

- Kahneman, D., & Tversky, A. (1979). Prospect Theory: An Analysis of Decision under Risk. Econometrica, 47(2), 263–291.

- Shefrin, H., & Statman, M. (1985). The Disposition to Sell Winners Too Early and Ride Losers Too Long: Theory and Evidence. The Journal of Finance, 40(3), 777–790.

- Banerjee, A. V. (1992). A Simple Model of Herd Behavior. The Quarterly Journal of Economics, 107(3), 797–817.

- Shiller, R. J. (2000). Irrational Exuberance. Princeton University Press.

- Tversky, A., & Kahneman, D. (1973). Availability: A Heuristic for Judging Frequency and Probability. Cognitive Psychology, 5(2), 207–232.

- Tversky, A., & Kahneman, D. (1981). The Framing of Decisions and the Psychology of Choice. Science, 211(4481), 453–458.

- Fischhoff, B. (1975). Hindsight ≠ Foresight: The Effect of Outcome Knowledge on Judgment Under Uncertainty. Journal of Experimental Psychology: Human Perception and Performance, 1(3), 288–299.

- Loomes, G., & Sugden, R. (1982). Regret Theory: An Alternative Theory of Rational Choice under Uncertainty. The Economic Journal, 92(368), 805–824.

- Babcock, L., & Loewenstein, G. (1997). Explaining Bargaining Impasse: The Role of Self-Serving Biases. Journal of Economic Perspectives, 11(1), 109–126.

- Thaler, R. (1980). Toward a Positive Theory of Consumer Choice. Journal of Economic Behavior & Organization, 1(1), 39–60.

Descubre más desde Irrational Investors

Suscríbete y recibe las últimas entradas en tu correo electrónico.