When the Market Prices Death, Who’s Actually Dying?

There is a moment in every disruption cycle or event when the market just price narratives. I think we are living through that moment right now. The SaaS index or the S&P 500 software and services index dropped a lot as new “free” capabilities were announced by the main AI companies. Adobe, Salesforce, ServiceNow, companies reporting strong earnings, expanding margins and growing revenues have been slashed greatly since 2024/2025 because the story the market is telling itself is simple, seductive and, in many cases, probably wrong, and that is that AI will destroy them.

The market is looking for the next Kodak or Blockbuster in every stock that has even a tangential connection to a business model that AI might someday threaten. The question is whether the market is actually identifying the next victim or it is panicking indiscriminately, selling everything that fits the narrative. Is the market handing patient investors the kind of asymmetric opportunities that define careers?

I think this could be the case in many cases. And the behavioral finance literature, the historical record, and a straightforward application of the reverse DCF all point in the same direction.

The Chegg Problem

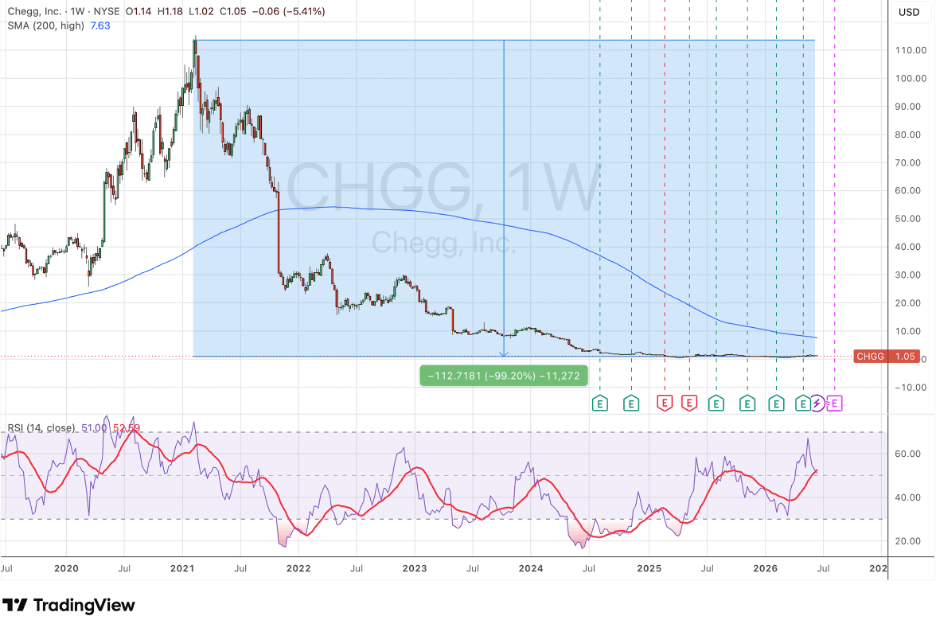

Chegg went from $113 per share and a $14.5 billion market cap in early 2021 to roughly $1 by early 2026. That’s 99% of its value, gone in 39 months, faster than Kodak and Blockbuster.

And the destruction was real. ChatGPT replicated Chegg’s core product (a database of homework answers) for free. Google’s AI Overviews choked off the organic search traffic that fed Chegg’s acquisition funnel. Students had no reason to pay $20 a month for a wrapper around technology they could access directly.

Chegg is a genuine binary casualty, but on the wrong side.

But here’s where the market goes off the rails, because it is now applying the Chegg reasoning to every company in its vicinity. Software companies with multi-year enterprise contracts, around 90% net revenue retention, and switching costs that would take a client years to unwind are being priced as if they were to lose them in the very short term. This is the representativeness bias that Kahneman and Tversky documented in 1974, the market sees a company with «software» in its description, sees that one software company was destroyed by AI, and concludes that the probability of destruction is high for all of them.

It could be…or not?

What the Research Actually Says

De Bondt and Thaler published their seminal paper in 1985 with a deceptively simple finding: stocks that experience extreme losses («losers») significantly outperform stocks with extreme gains («winners») over the subsequent three to five years. The effect was robust, persistent, and statistically significant. Translated into plain language, the market systematically overreacts to bad news, pushes prices below fundamental value, and then mean-reverts.

Forty years later, the mechanism hasn’t changed. Why? Some behavioral biases could help to understand it:

- Representativeness. Analysts and investors judge companies by how they appear rather than how likely the implied outcome actually is. They see declining revenue and extrapolate the decline indefinitely. Growth isn’t persistent. Neither is decline. Fama and French (2000) found that the rate of mean reversion is higher when profitability is far from its mean. The companies most beaten down are, statistically, the most likely to recover. Not all of them will. But the base rate favors recovery, not extinction.

- Narrative anchoring. Montier’s work on anchoring is pretty relevant here. In the current AI cycle, the anchor isn’t a number; it’s a story: «AI will destroy X.» Once the story anchors, the analyst’s target price gravitates toward the narrative conclusion, not toward the cash flows. The reverse DCF exists precisely to strip this away. Take the price, solve for the implied perpetual growth rate, and ask if this number makes any sense.

- Institutional herding. Dasgupta, Prat, and Verardo (2006) documented a 17% return differential between stocks persistently sold by institutions and stocks persistently bought. Seventeen percent over two years. The stocks that fund managers dumped most aggressively outperformed the market by 11%. The ones they bought most enthusiastically underperformed by 6%. In a selloff driven by narrative, institutional herding intensifies, compliance flags the sector, risk models flash warnings, portfolio managers trim, and the selling feeds on itself.

The implication is clear, the consensus trade in «short AI-disrupted companies» has become exactly the kind of crowded, one-way position that historically precedes violent reversals.

Same Movie, Different Decade

Every major technology disruption or event in the past thirty years has produced similar patterns. The details could change, but the behavioral dynamics are the same.

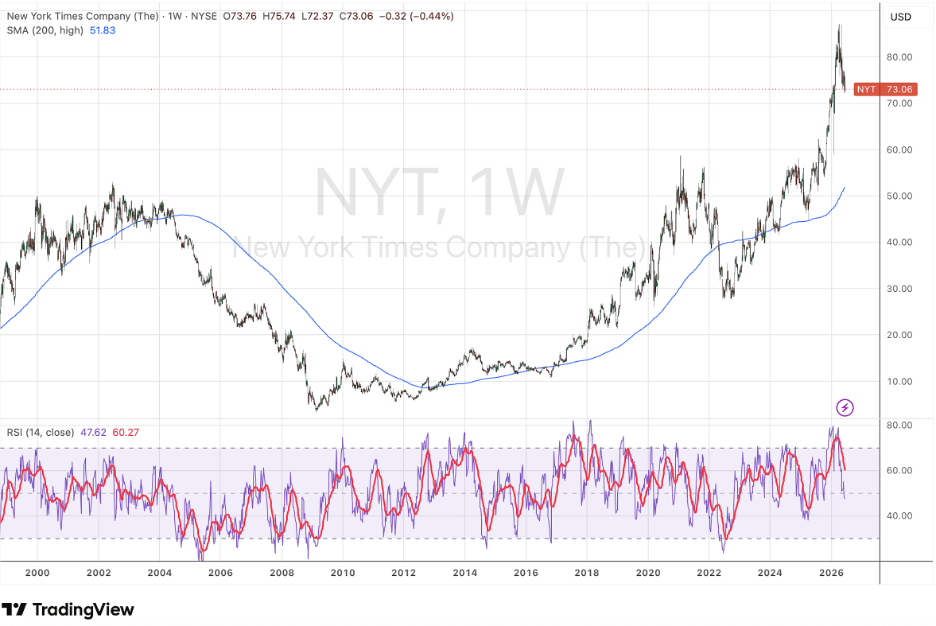

Newspapers and the internet. The New York Times fell from $50 to under $4 between 2002 and 2009. At $4, the market was pricing in the death of premium journalism. The company was still generating free cash flow, had a globally recognized brand, and possessed investigative infrastructure that no blog or aggregator could replicate. The binary question was whether differentiated journalism survives digital disruption. The market spoke and said yes. The NYT reinvented itself around digital subscriptions and the stock recovered past $50. A 12x return for anyone who correctly assessed the probability.

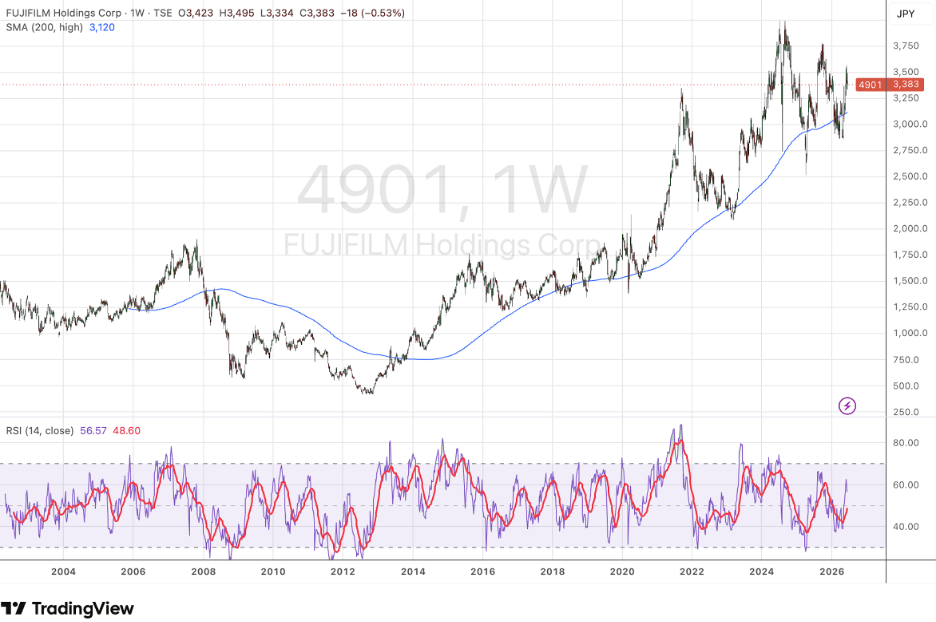

Kodak vs. Fujifilm. Two companies with identical disruption but opposite outcomes. Both derived the majority of their revenue from photographic film, which collapsed at 20-30% per year. The market priced both for death. Kodak, anchored to its film supply chain, filed for bankruptcy in January 2012 with $6.75 billion in debt. That same year, Fujifilm posted record revenues exceeding $21 billion, having diversified into document solutions, healthcare imaging, and advanced materials. The narrative was identical when the fundamentals were not. The questions the analyst should ask, without being influenced by the trend, were whether management’s response to disruption will take advantage of the company’s core competencies to build new businesses (Fujifilm) or whether it will try to defend a dying business model with half-measures (Kodak).

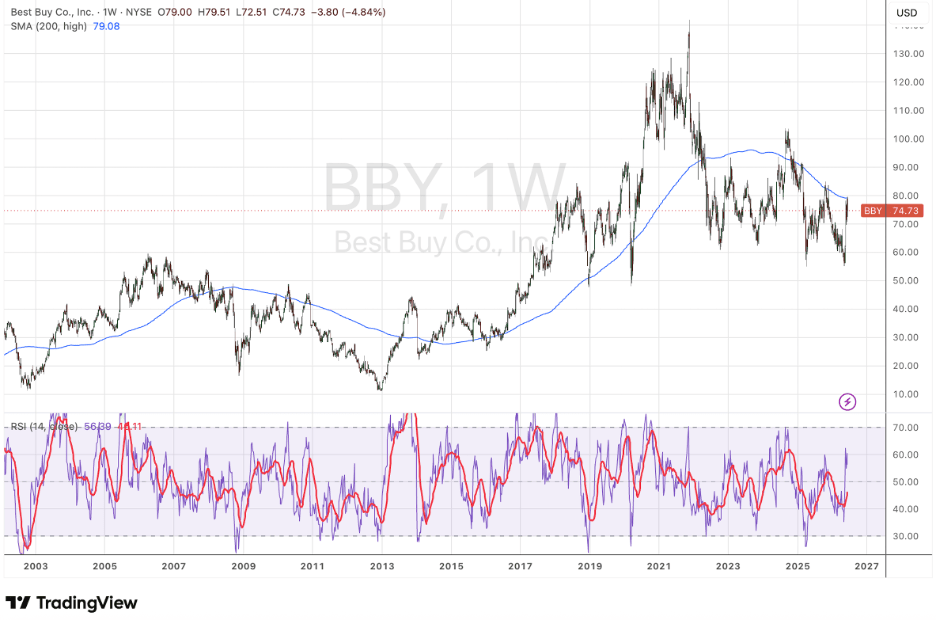

Best Buy and the «retail apocalypse.» Left for dead at $12 in 2012 amid predictions that it would become nothing more than an Amazon showroom, it starred a turnaround and the stock exceeded $130 by 2021. A 5x return from the trough. The market correctly identified the general threat to brick-and-mortar retail but failed to discriminate between commodity retailers (who were genuinely vulnerable) and differentiated platforms (who could adapt).

The 2008 financial crisis. The market priced ALL financials for death. But the outcomes diverged dramatically. Richard Pzena loaded up on Freddie Mac, Fannie Mae, and Citigroup, and was destroyed. These were the businesses where the structural impairment was real. But the investors who bought JPMorgan at $15 (Jamie Dimon was buying JPM shares with his own money at $22), Goldman Sachs at $47, or Bank of America at $3 during the same panic, when the «end of capitalism» narrative was at its peak, earned 5x to 10x over the following decade. Same crisis, same narrative, opposite outcomes. The lesson is not «don’t buy during panics», it is that being cheap is necessary but not sufficient. Being cheap and structurally sound is the trade.

The pattern repeats because the behavioral mechanisms that produce it (representativeness, extrapolation, herding, fear asymmetry) are hardwired into human cognition. They don’t disappear with new technology, they could intensify, because new technology comes wrapped in compelling narratives that make the biases feel rational.

The Binary Opportunity

What is then a «binary opportunity»:

A stock whose price implies one of two outcomes, survival or extinction, with virtually no middle ground priced in. The payoff structure is fundamentally asymmetric; if the company survives and adapts, the upside is huge, because the market was pricing terminal decline, not slower growth. The downside, while theoretically total, is already substantially reflected in the price.

But not every cheap stock in an AI-threatened sector is a binary opportunity. Some of them are genuinely going to zero (ask Chegg’s shareholders…). The framework requires 5 diagnostic questions:

1. Moat architecture. Can AI replicate the competitive advantage? Chegg’s moat was a homework database, easily replicable. Vertical market software that encodes decades of regulatory compliance, workflow logic, and customer-specific configuration is a different beast entirely. If the moat lives in content, AI can eat it, but if the moat lives in relationships, regulatory embedding, or physical infrastructure, AI probably can’t … at least for the moment.

2. Revenue stickiness. Is the revenue contractual or not? Chegg depended on Google organic search. When Google’s AI Overviews appeared, the acquisition funnel died at the source. Companies with multi-year enterprise contracts and more than 90% net retention face a different problem entirely, their clients can’t leave in the short term, even if they want to.

3. Management’s strategic response. Is management using AI to enhance the existing business (deepening switching costs, automating internal processes, creating new features), or are they trying to wrap AI around a dying product? Building an AI layer that makes your entrenched software more valuable is the Fujifilm response.

4. Strong Balance Sheet. Can the company survive long enough for the binary to resolve? Net cash, positive free cash flow, and no approaching debt maturities constitute the margin of safety in a binary setup. Cash buys time and time buys optionality.

5. Reverse DCF implied growth. The quantitative anchor. If the current implied g is deeply negative, the market is embedding a permanent annual contraction. Is that plausible for this specific business? In most cases, the answer is no, which means the expected value of the position is positive.

Conclusion

Humans extrapolate narratives with the same fervor they extrapolate growth rates. When AI destroys one homework-answer company, the market extrapolates that AI will destroy every software company. When one newspaper dies, every newspaper stock goes to zero. When one retailer liquidates, almost the entire sector is written off.

But mean reversion is the dominant force in corporate profitability and the companies most beaten down by narrative are often the ones where mean reversion will be most powerful, if they survive… The five diagnostics exist to assess that «if.» The reverse DCF is an excellent tool to quantify the embedded narrative and test it against reality.

Morgan Stanley published a note in March 2026 arguing that AI disruption fears were overblown. LPL Financial pointed out that even after the worst round of EPS cuts since December 2018, software earnings were still expected to grow 25% in 2026 with operating margins expanding from 23% to 39%. The selloff was driven by story, not by cash flows. Meanwhile, software valuations hit three-year lows.

We’ve seen this movie before with different players, AI instead of the internet, language models instead of digital cameras, but the behavioral script is identical. The market is pricing extinction across a broad swath of businesses where the actual probability of survival could be high for some of them.

AI will disrupt industries for sure, but the question is which companies the market has condemned to death that will actually survive.

In the answer is where the «Xx» returns live, and that’s where we’re looking.

Disclaimer:

We wrote this article ourselves, and it reflects our own opinions. We did not receive compensation for it. We have no business relationship with any company whose stock is mentioned in this article.

The views contained in this document are for informational and educational purposes only, and should not be construed as a recommendation to buy or sell any of the securities mentioned, or as a solicitation of transactions or clients. Past performance is not indicative of future results. Investments in equities carry risks, including loss of principal. The analysis is based on data available as of December 5, 2025. The information contained herein is believed to be appropriate; however, under no circumstances should any person act solely based on the information provided. We do not recommend that anyone act on any investment information without first consulting an investment advisor regarding the suitability of such investments for their specific situation.

Irrational Investors and/or its affiliates may hold a position in the securities mentioned in this report and may make purchases or sales of such securities from time to time in the open market or otherwise. The analyst primarily responsible for this report may also hold a personal position in the subject securities.

Descubre más desde Irrational Investors

Suscríbete y recibe las últimas entradas en tu correo electrónico.