A FOLLOW-UP ANALYSIS ON CROCS, INC. (NASDAQ: CROX)

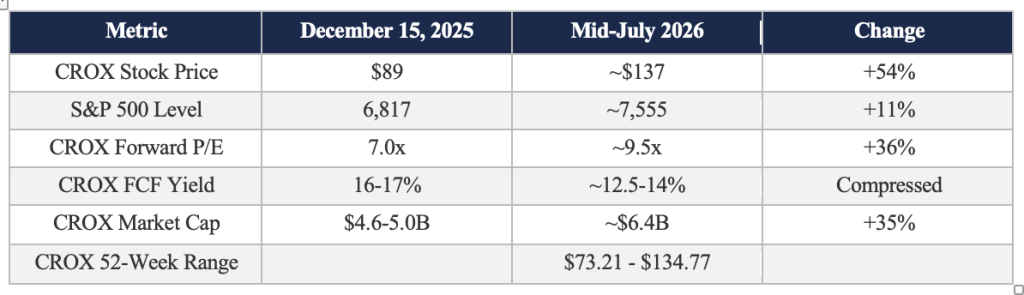

Seven months ago, when Crocs was trading at about $89, we wrote an article saying that the market had become too pessimistic, even though HEYDUDE was clearly struggling, North American demand was soft and tariffs added another layer of uncertainty. We thought that the market was already assuming that these problems would last indefinitely. At around 7 times forward earnings and a 16–17% FCF yield on our normalized assumptions, our thesis was then that very little had to go right for the shares to work.

Our conservative sum-of-the-parts valuation was $127 per share even after assigning no value to HEYDUDE. The central DCF produced $163, the more optimistic case $193, and we settled on $145 as a reasonable target. We described the stock as a possible deep-value opportunity, although one with enough obvious problems to qualify as a potential value trap.

The value-trap question has now largely been answered. The more difficult question is what to do after the market has answered it for us.

A 54% return in seven months

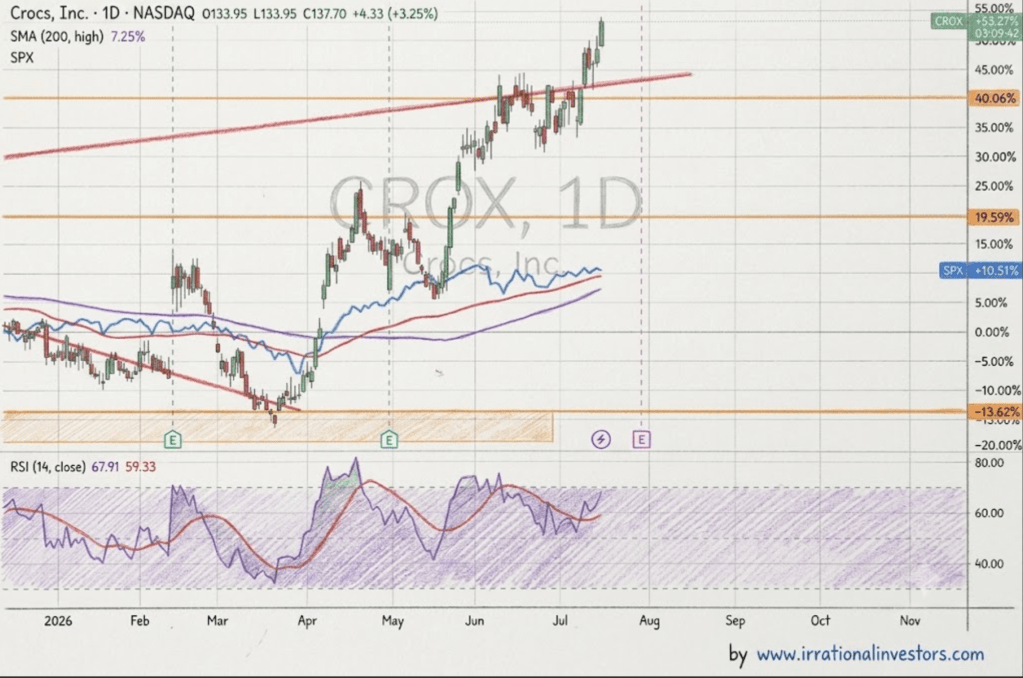

CROX closed at $89.70 on December 15, 2025. On July 16, 2026, it was trading at around $137, giving shareholders a return of about 54%. Over the same period, the S&P 500 rose approximately 11%, so CROX outperformed the index by roughly 43 percentage points.

The path was anything but smooth, the shares first fell to a 52-week low of $73.21 before rebounding by almost 88% to their present level.

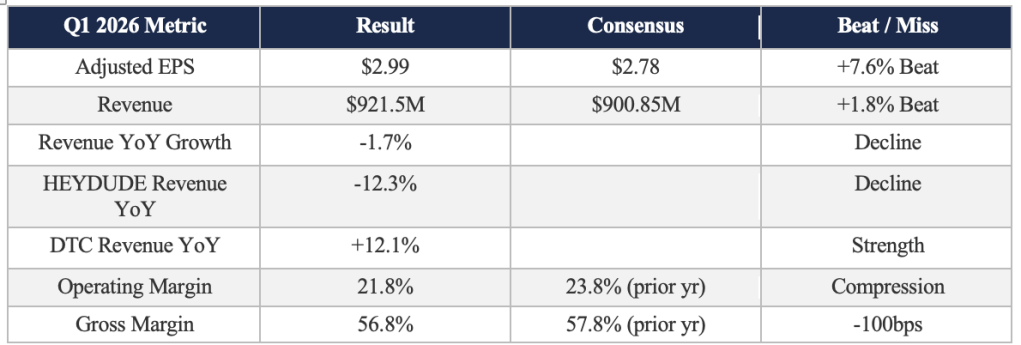

The main catalyst was the first-quarter results on April 30, where Crocs reported revenues of $921.5 million and adjusted EPS of $2.99, compared with consensus expectations of approximately $900.8 million and $2.78. Management also raised full-year adjusted EPS guidance from $12.88–$13.35 to $13.20–$13.75.

It was a better quarter than the market expected, however, it wasn´t a dramatic acceleration in the underlying business. Consolidated revenue still declined 1.7% year on year and 4.0% in constant currency, the volume decline was 7.2%, higher average selling prices added 3.2% and favourable currencies another 2.3%. In other words, the reported number benefited from pricing, mix and foreign exchange while the company sold fewer units.

There were encouraging signs underneath that headline. Company-wide direct-to-consumer (DTC) revenue increased 12.1% (DTC revenue for the Crocs brand grew 12.9%), international Crocs-brand revenue increased 7.2% to $421 million, comfortably ahead of the $346 million generated in North America, where sales fell 6.1%.

Total borrowings declined to $1.34 billion from $1.48 billion a year earlier. After the quarter closed, Crocs also repurchased 0.8 million shares for $73.6 million, leaving $673.2 million under its existing authorization.

Those were positive signs as international growth is reducing the company’s dependence on North America, the DTC channel is performing well, leverage continues to come down and management is returning cash at prices it evidently considers attractive.

HEYDUDE is still a huge concern

The weaker side of the story remains familiar. HEYDUDE revenue fell 12.3% to $154 million and its wholesale revenue dropped 24.7%. Segment operating income declined 31% to only $16 million. Even the Crocs brand itself grew reported revenue by just 0.8% (declined 1.9% in constant currency) while its operating income fell 7.5%.

At group level, gross margin declined from 57.8% to 56.8% and operating margin fell from 23.8% to 21.8%. The 10-Q attributes the gross-margin pressure mainly to incremental duties and an unfavourable product mix, partly offset by pricing.

These figures do not describe a company in distress, but neither do they describe the sort of earnings inflection that normally explains a 53% share-price increase.

The outstanding litigation also deserves a measured mention. Crocs is defending a securities class action and several derivative actions relating to wholesaler inventory and its alleged effect on reported revenue. The company says it cannot currently estimate the potential loss from those cases. Its $1.7 million legal accrual covers legal claims and disputes generally, so it should not be interpreted as Crocs’ estimate of the eventual cost of this particular litigation. For now, we view this mainly as headline risk rather than the central reason to sell the shares, but it is not something to ignore. (Crocs Q1 2026 Form 10-Q, Note 14)

The company improved a little, bu the valuation changed a lot

At approximately $137, Crocs has an equity value of about $7.0 billion. Using the midpoint of management’s $13.20–$13.75 adjusted EPS guidance, the stock trades at roughly 10.2 times expected 2026 earnings.

That is hardly an excessive multiple for a business with the profitability and cash-generating capacity of the Crocs brand. It is simply much less exceptional than the price in December.

The same applies to free cash flow. Crocs generated $710.4 million of operating cash flow in 2025 and spent $51.2 million on property, equipment and software, producing reported free cash flow of approximately $659.2 million. Against the current market capitalization, that is a trailing free-cash-flow yield of about 9.5%. If we instead use the $800–900 million normalized range from our original analysis, the yield is approximately 11.5–13.0%.

Not bad but neither reproduces the 16–17% opportunity available at the december price.

It is also useful to revisit our own valuation rather than quietly moving the goalposts after a successful call. The shares have already passed the $127 conservative SOTP value. From $137, the original $145 target offers only about 6% upside. The $163 central DCF offers approximately 19%, while reaching the $193 optimistic case would require another 41%.

The FCF growth implicit in the current price has changed dramatically, from around a negative 4% to a positive 1%.

The central valuation still suggests some upside, but enough to compensate for forecast risk, brand risk and the possibility that the market changes its mind?

At $89, the valuation itself absorbed a considerable amount of bad news. At $137, the investor is relying much more heavily on the operating assumptions being right. The earnings outlook has improved, but most of the return has come from investors agreeing to pay a higher multiple for those earnings.

The analyst upgrades

Sell-side opinion has become more positive as the shares have recovered. In June, Piper Sandler upgraded CROX from Neutral to Overweight and increased its target from $95 to $150. Baird moved from Neutral to Outperform and raised its target from $115 to $150. BofA increased its target to $145, Williams Trading to $150, and Stifel raised its target from $105 to $125 while retaining a Hold rating.

The upgrades confirm that sentiment has improved, just that. Still, the targets need to be read in the context of the current price. A $145 target now represents only around 6% upside.

There is also a near-term test approaching. Crocs will report second-quarter results on July 30. Management currently expects group revenue to decline slightly, Crocs-brand revenue to grow by approximately 1–3%, and HEYDUDE to decline by 12–14%. Adjusted EPS is expected to be $4.15–$4.35, with an adjusted operating margin of approximately 24.7%.

After such a rapid share-price move, merely meeting those numbers may not be enough to generate another rerating.

What to do now

After the recent rally, this could be a good moment to reduce some exposure at the current price. A complete exit could also be reasonable for an investor whose thesis was primarily based on mean reversion, as the conservative valuation has been exceeded, the original target is close, and a great deal of the rerating has already occurred.

A long-term shareholder with greater confidence in international expansion and the durability of the Crocs brand could keep a position. That is a defensible choice, but it should be understood as a different investment strategy from the one in December. The new strategy at these prices requires continued international growth, stable brand relevance, disciplined capital allocation and, eventually, evidence that HEYDUDE can stop shrinking. The original strategy did not require all of those things to go perfectly well.

Crocs remains a very good business built around one exceptional brand and one disappointing acquisition that must still be fixed. The stock is reasonably valued, but it is no longer the same bargain.

The ugly shoe turned out to be a beautiful trade. The question now is not about the shoe or the story, it is about how expensive or cheap it is.

In any case, and as always… Judge for yourselves.

Disclaimer

We wrote this article ourselves, and it reflects our own opinions. We did not receive compensation for it. We have no business relationship with any company whose stock is mentioned in this article.

The views contained in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell any of the securities mentioned, or as a solicitation of transactions or clients. Past performance is not indicative of future results. Investments in equities carry risks, including loss of principal. The analysis is based on data available as of July 16, 2026. The information contained herein is believed to be appropriate; however, under no circumstances should any person act solely based on the information provided. We do not recommend that anyone act on any investment information without first consulting an investment advisor regarding the suitability of such investments for their specific situation.

Irrational Investors and/or its affiliates may hold a position in the securities mentioned in this report and may make purchases or sales of such securities from time to time in the open market or otherwise. The analyst primarily responsible for this report may also hold a personal position in the subject securities.

Irrational Investors Research

Descubre más desde Irrational Investors

Suscríbete y recibe las últimas entradas en tu correo electrónico.